Two Approaches, One Goal

What if you could erase your credit card processing fees by adding a small surcharge to every purchase that your customers make?

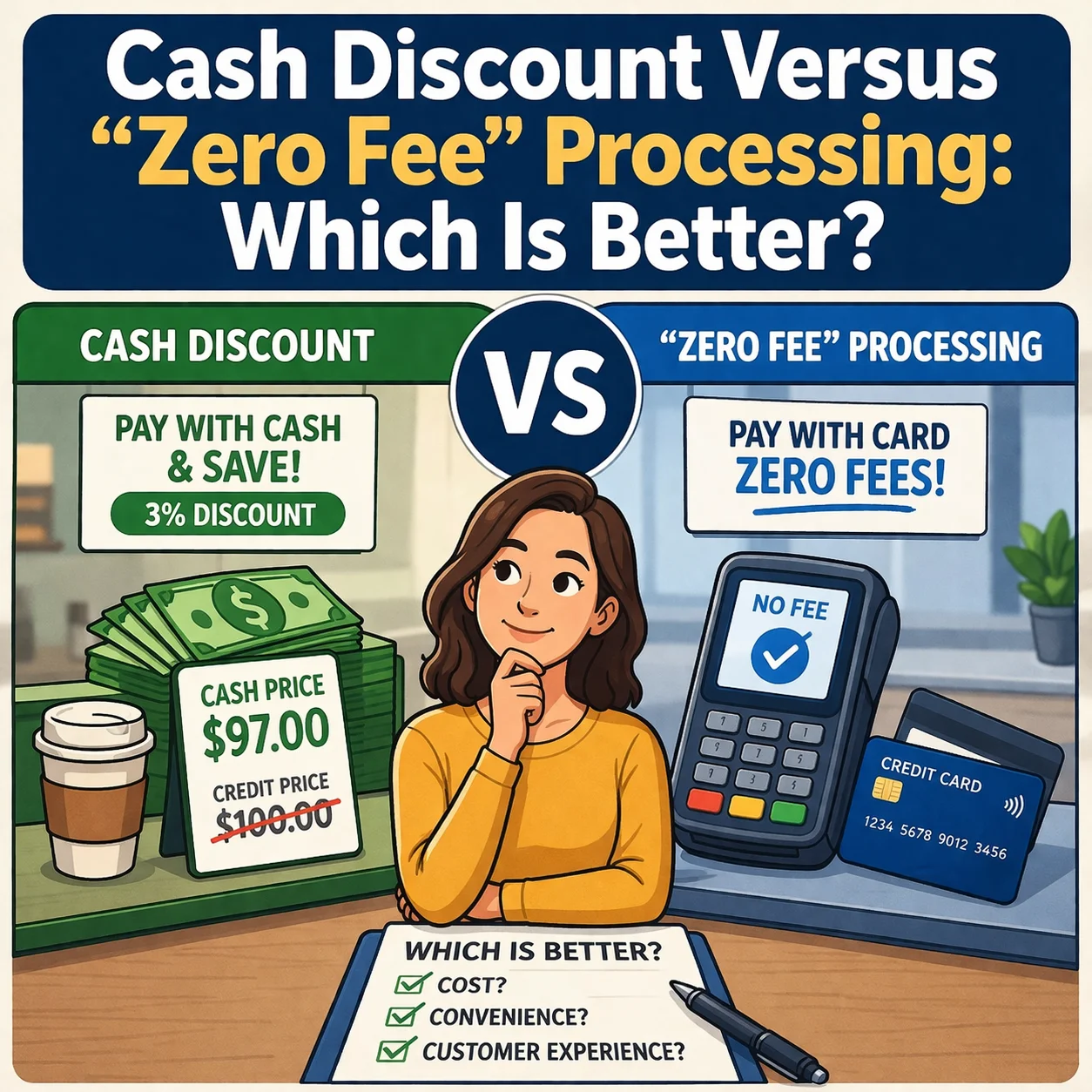

Two new pricing models that promise to do just that are gaining popularity in the credit card processing industry: cash discount programs and zero fee processing. Both programs promise big savings for merchants—sometimes even advertising “free” credit card processing—and both impose surcharges on certain types of purchases to help offset the transaction fees that are charged to merchants. However, there are some key differences between these models, and each comes with its own benefits and drawbacks. If you have been approached by a salesperson advertising one of these pricing models, or if your current merchant account provider has offered one of these plans to you, then you should read on to determine whether a cash discount program or zero fee processing is right for you.

What’s The Difference?

First, it’s important to understand how each pricing plan works. The particulars will vary from provider to provider, but the basic structure of each plan is as follows:

A cash discount program adds a fixed surcharge to the price of every product in a merchant’s store and then waives that surcharge for customers who pay with cash. In other words, all non-cash transactions will come with an extra surcharge, usually between 1% and 4%, and the revenues generated by this surcharge are used to offset the merchant’s costs for accepting electronic payments. Customers who pay with cash receive the discount, while customers who pay with any non-cash method effectively have the cost of processing their payments passed down to them.

Zero fee processing, also called “reverse fee” processing or simply “free” processing, adds a fixed surcharge to credit card transactions only. Customers who pay with cash, check, debit, or any other non-credit option will not pay this surcharge. Due to legal restrictions, this surcharge cannot exceed 4%. Like a cash discount program, however, it is designed to offset the merchant’s credit card processing costs by passing costs on to credit card-using customers.

These pricing models are just now beginning to gain widespread traction, so it’s not uncommon to see some payment processors use the terms interchangeably. However, there are very important distinctions to be made between the two practices.

Cash discount programs have been legally used by some merchants for more than a decade. As long as merchants properly disclose their surcharges and apply a surcharge to all non-cash options without discriminating between non-cash options, they will be fully compliant with industry regulations.

The selective surcharges added under zero fee processing, however, have been the subject of multiple legal disputes between retailers and the major card networks. At this time, credit card surcharges are still illegal in California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma, Texas, and Puerto Rico. In states where surcharges are legal, they cannot be applied to debit transactions, they cannot exceed 4%, and they cannot be charged without a full 30 days’ advance notice provided to customers via in-store signs.

From a certain perspective, this entire issue seems like a silly battle of semantics. After all, what’s the difference between adding a surcharge to credit card transactions and offering a discount to customers that pay in cash? Well, in the eyes of the card associations, it’s a very real difference that you’d be foolish to ignore. If you are interested in either plan, be sure to specifically ask your sales representative which of the two plans they are marketing.

Other Considerations

The basic appeal of cash discounts and zero fee processing is that you can earn back your processing fees by charging your customers a couple extra percentage points on credit card transactions. However, you can’t do this secretly. Both approaches require you to disclose to your customers that you are charging them more for using a credit card. Depending on your industry and your competition, this may leave a sour taste in your customers’ mouths or drive them to competitors. Cash is losing popularity as a payment option, and customers might resent that you’re asking them to compensate you for what has traditionally been a normal cost of doing business.

Another thing to keep in mind is that zero cost processing doesn’t necessarily mean that your merchant account will be free overall. In addition to per-transaction fees, most credit card processors charge one-time, monthly, and incidental fees such as monthly minimum fees, chargeback fees, PCI compliance fees, and early termination fees. A surcharge of 4% on certain transactions might help to make up for transaction fees, but it probably won’t do much to cut into other monthly fees.

Finally, you should understand that the legality of credit card surcharges has been the subject of multiple lawsuits and isn’t firmly settled throughout the country at this point. Federal law explicitly allows merchants to offer cash discount programs, but surcharges still aren’t legal in every state. If you choose to set up a surcharge program at your store, you will need to stay informed on any possible changes to the regulations that govern this practice.

So Which Is Better?

Due to its firmly established legal status, a cash discount program is preferable to zero fee processing in our view. Not only are cash discounts easier to implement and explain to customers, they are the only way for merchants to offset their debit card transaction fees in addition to their credit card transaction fees. Zero fee processing only applies to credit card transactions.

Zero fee processing is still an interesting approach to pricing, and providers are currently developing some creative products and services designed to apply surcharges within the bounds of the law. However, the surcharge-based approach involves the same drawbacks as cash discounts (customer dissatisfaction, disclosure issues) with far less flexibility or earning potential.

For the time being, merchants who are willing to charge non-cash customers more than cash customers will be better off using a cash discount program.

A Third Option

Although these programs represent an innovative pricing approach for the credit card processing industry, they gloss over an important fact: you can always save money on your merchant account without passing costs on to your customers. Whether you need to negotiate better pricing, switch to a highly rated provider, or learn more about rates and fees, there are plenty of ways for you to minimize your payment processing costs on your own. Before you pass exorbitant costs on to your customers, you’d be smart to look upstream first and make sure your provider is treating you fairly.