In this article, we'll provide an in-depth analysis of WePay, a payment processing service that has undergone significant changes since its acquisition by JPMorgan Chase in 2017. Initially a competitor to services like Stripe, WePay has transformed into a white-label payment platform focusing on online marketplaces and fundraising systems.

We will explore the key features of WePay’s services, including its various payment gateways – Clear, Link, and Core – and how they cater to different business needs, such as credit and debit card processing, bank transfers, and digital wallet options. This article will also highlight WePay's virtual terminal, mobile payment solutions, and API integrations, which are crucial for businesses seeking a seamless payment experience.

A significant part of our discussion will address customer concerns, particularly regarding fund holds and customer service issues, drawing on user reviews and industry ratings to provide a comprehensive understanding of WePay's performance in these areas. Additionally, we will delve into the financial aspects, such as fees, rates, and contract terms, including an analysis of WePay's policies on holding funds.

Concluding with an overall assessment, this article aims to present a balanced view of WePay, helping businesses and developers make informed decisions about utilizing this payment processing platform.

About WePay

Founded in 2008, WePay is a merchant account alternative that first started as a competitor to services like Stripe. The company has been assimilated into the Chase Merchant Services brand. The company's primary focus is providing online platforms with the ability to collect payments from customers and donors (for example, through websites like GoFundMe.com). WePay allows virtually any website to integrate an account to collect payments from participating users via ACH bank transfers and credit cards. The service has no setup fees, no monthly fees, and no service length requirement.

Is WePay Holding Your Funds Right Now?

Thousands of business owners have had their payments frozen by WePay. If you're one of them, then you might find these resources helpful:

Over the last few years, WePay has changed its branding to present itself as a white-label payment platform that can be integrated into an existing e-commerce store or utilized as the backend platform for an online marketplace or fundraising system. This makes it less of a peer-to-peer or business-to-consumer service and more of a backend software solution for payment-oriented businesses and startups. In fact, the company is considered one of the top payment processors for online marketplaces. This newly emphasized function makes the company less relevant for most types of small business owners. In October 2017, JPMorgan Chase acquired WePay.

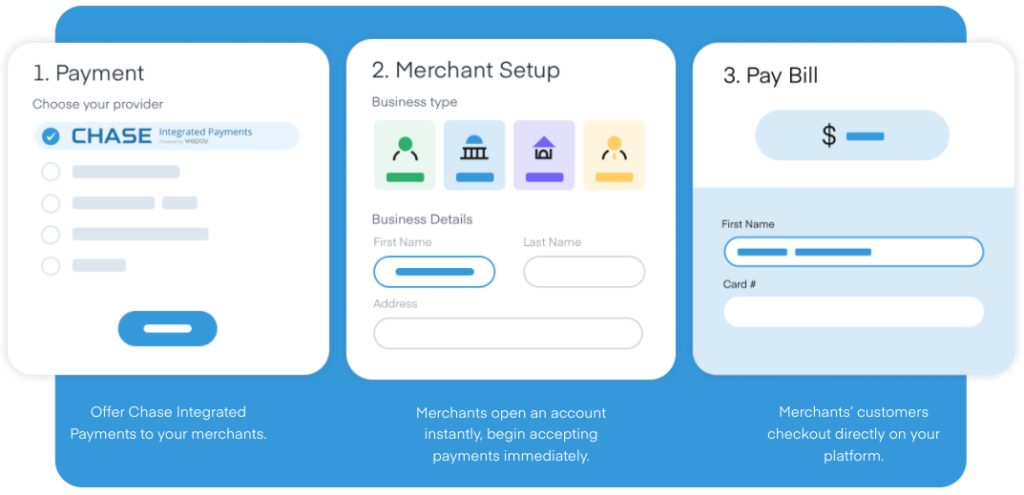

WePay, in partnership with Chase bank, offers three different payment gateways for online businesses. The first option, Clear, provides a basic payment gateway along with risk management solutions. The second option, Link, connects directly to Chase's processing and uses the Chase name. Both Clear and Link include features such as same-day deposits, digital wallets, card-present solutions, PCI compliance, card vaults, tokenization, and data reporting and analysis. The third option, Core, is designed for large-scale payment facilitators.

Payment Processing

WePay's payment processing service supports multiple payment methods, including credit and debit cards, bank transfers, and digital wallets. The platform integrates various payment gateways, offering a streamlined payment processing experience.

Virtual Terminal

WePay offers a virtual terminal that allows businesses to accept payments over the phone or via email. This online payment processing platform enables businesses to process payments from any device with an internet connection.

Mobile Payments

WePay supports mobile payment processing, enabling businesses to accept payments through smartphones and tablets. The platform is compatible with both iOS and Android devices and includes a mobile SDK for app developers.

Recurring Payments

WePay's recurring payment service allows businesses to set up automated payments for customers, making it ideal for subscription-based services or products.

E-commerce Solutions

WePay provides e-commerce solutions that support businesses in selling products and services online. The platform integrates with several e-commerce platforms, including Shopify, WooCommerce, and BigCommerce.

WePay Risk and Fraud Protection

WePay offers risk and fraud protection using advanced data analytics and machine learning to identify and prevent fraudulent transactions, safeguarding businesses and their customers.

WePay API Integrations

WePay provides API integrations that allow businesses to embed the payment service directly into their applications or websites, enabling a seamless transaction experience without customers needing to leave the business platform.

WePay's link payment processing option

WePay Customer Reviews

Here's What Their Clients Say

Customer Reviews Summary

Total Online Complaints

500+

Live Customer Support

Yes

Most Common Complaint

Fund-Holds

Recent Lawsuits

No

Issues with Fund Holds

In the comments section of this review alone, we’ve uncovered over 300 WePay reviews, with many users labeling the company as a scam or ripoff. Additionally, nearly 200 complaints are found on other consumer protection websites. The predominant concerns across these reviews include WePay’s reserve policy, its “prohibited activities” policy, and difficulties in reaching helpful customer support. Numerous business owners report waiting the full 30 days to access significant portions of large payments held in reserve. We invite you to share your own WePay review in the comments below.

Lack of Effective Communication

While it’s common for processors to implement fraud prevention measures like fund holds, there appears to be inadequate warning or communication from WePay to its clients in such cases. Similarly, businesses often discover account cancellations and pending payment returns only after reaching out to WePay for clarification on missing funds. Many business owners express frustration with WePay’s customer support, available via phone or live chat, citing unhelpful assistance and a tendency to deflect issues.

Subpar Performance and Support

While a company representative has been actively responding to complaints in the comments, it appears that most clients’ concerns remain unresolved to their satisfaction. Overall, negative WePay reviews consistently highlight dissatisfaction with the company’s customer service.

WePay Legal Status and Customer Support

At present, there are no outstanding class-action lawsuits or FTC complaints against WePay. Dissatisfied business owners seeking alternatives to litigation can consider reporting issues to relevant supervisory organizations.

Customer Support Channels

WePay exclusively offers ticket support through its website, available from 9 am to 9 pm EST. The company commits to responding to all requests within 1 business day. However, its limited support options prevent it from being ranked among the top merchant account providers for customer service.

WePay has a low customer review rating of 1.02/5 stars on the Better Business Bureau (BBB) website, based on 66 customer reviews. The company has also received 169 complaints closed in the last 3 years, with 95 complaints closed in the last 12 months. Common themes in the reviews and complaints include issues with customer service, problems with product or service, and difficulties in processing payments.

Negative Feedback

This company is randomly holding our money after significantly long periods of time stating reasons of ‘compliance’ after a client has undergone micro-deposit verification and our accounts have remained constant for over a year. They asked me to send them my bank statements and take photos of me next to my ID. It’s all a smoke screen for how to hold our money for longer. This is happening to multiple owners of other **************** Franchisees causing massive delays in our deposits. I own **************** *********** and this is absurd. Zelle, PayPal, VenMo and tons of other financial institutions work with us to do on a daily basis.

– Complaint from October 24, 2023

Scam. Stay away. They hold money for no reason and have no phone support. ***** needs to get rid of this Chinese espionage of a company taking small business owners’ money.

– Review from November 17, 2023

Positive Feedback

There are no positive reviews published about WePay on the BBB website.

WePay has an average customer review rating of 1.2 stars on Trustpilot based on 774 customer reviews. Common themes in the reviews include complaints about funds being held for extended periods, poor customer service, and issues with account closures.

Negative Feedback

Businesses beware!!! For some reason, they are holding all transactions for all clients for 120 days. Been using them for over 2 years with no disputes or chargebacks, but for some reason started this October, they started holding all transactions for 120 days. Class Act in the works.

– Review from November 14, 2023

Chase/WePay is inducing consumers with their intentionally vague terms and conditions, closing accounts, and stealing money for up to 120 days to use in their Ponzi scheme. Their reason? “That’s proprietary information”. Just look at the hundreds of reviews of other people this has happened to. This scheming is ripe for a Class Action Lawsuit and I hope and pray this gets picked up.

– Review from October 12, 2023

Positive Feedback

There are no positive reviews published about WePay on the Trustpilot website.

WePay has an average customer review rating of 1.1 stars on PissedConsumer based on 54 customer reviews. The majority of reviews are negative, with common themes including poor customer service, issues with payments and charges, and difficulties in communication with the company.

Negative Feedback

Will not release my funds. Demand info already provided. They say they will release funds, then retract. No way to easily contact them. No phone number. Absolutely the worst customer service. Meanwhile, they owe me over 6k. – Review from November 16, 2023

Absolutely horrible. Would not ever use again. Our small business Used WePay for only days to try it out. Had a chargeback request from a customer. First one in thousands of transactions/sales after 14 years in business. WePay asked to concede or challenge. I challenged as we have proof that goods and services were 100% delivered and used for duration of event. We provided full documentation limited to 5. They did not respond and have pulled monies from our account back to customer. We are justified as a business and now are looking at small claims court option as Chase WePay could not have properly read the documents and sides with client in the wrong. The lack of communication and proper evaluation is beyond frustrating and now very costly. We were never given a reason for the chargeback or the decision. I’ve reached out to Chase WePay on our ticket number and was told to reach out to another company, who does not have access to banking or the authority to manage transactions. VERY FRUSTRATING and incredibly unjust. – Review from September 5, 2023

Positive Feedback

There are no positive reviews published about WePay on the PissedConsumer website.

WePay no longer displays per-transaction fees on its website. Previously, it listed rates of 2.9% + $0.25 for credit card payments by new U.S. businesses or 1% + $0.30 for direct bank account payments. It’s now likely that it customizes pricing for each payment platform it partners with. Apart from flat processing rates, WePay’s site notes a $15 chargeback fee, standard in the industry. However, some of its policies, notably regarding reserves and prohibited activities, remain ambiguous.

WePay’s Former Hold Policy

Previously, WePay implemented a standard withdrawal limit of $2,500 per business per seven days, with amounts above held in a rolling 30-day reserve. Although this policy is no longer in WePay’s terms, the company retains the right to impose transaction limits at its discretion.

WePay’s Current Hold Policy

Reserve amounts are determined by various factors, including transaction history, profile information, industry, and usage patterns, according to previous website content. While fund withholding is common in the industry, WePay’s failure to adequately notify clients about approaching or exceeded withdrawal limits leads to frustration among business owners.

Inadequate Screening

WePay seems to lack robust screening processes for prohibited industries until after clients have begun processing. Accounts in such industries are often canceled without sufficient warning, leaving businesses without expected funds. Businesses in these categories may benefit from specialized high-risk specialists.

Revised Approach, Persistent Issues

WePay asserts that partner platforms are now responsible for screening out prohibited businesses, reducing complaints about fund holds and account cancellations. However, this reliance on partner platforms raises concerns about improper business approvals and potential cash flow disruptions. We also recommend exploring our list of the best merchant accounts.

WePay primarily uses its website to market itself as a payment solution for online platforms. That said, the website formerly quoted two rates: 2.9% + $0.30 for credit card payments or 1% + $0.30 for direct payments from bank accounts. These rates appear to be accurately quoted and inclusive. The website now only quotes one rate: 2.9% + $0.25 for credit card payments valid for new U.S. businesses only. Additionally, the company does not appear to engage in any deceptive advertising strategies in its official materials. This compares favorably to our list of best credit card processors.

A History of Holding Funds

By far the most common complaints about WePay are older complaints filed when the company was marketing itself to all businesses. These complaints were related to its policies regarding reserves and high-risk merchant accounts. These issues could be characterized as either sales issues or service issues. To the extent that they were related to sales and marketing, it seems that the company’s application/setup process did not do an adequate job of screening out businesses that would ultimately have their account terminated after they had been allowed to process transactions. We were able to locate numerous WePay reviews by clients who were told by either the company’s website or one of its representatives that their business type qualified for processing through WePay, only to find out after processing large payments that their accounts had been canceled and their funds returned to customers. It seems that this common issue could have been more easily avoided if the process for signing up for a WePay account were a more thorough and guided one.

No Longer Selling Directly to Businesses

WePay claims that its current focus on crowdfunding platforms and marketplace websites has eliminated most complaints of this nature. The feedback we have received does not corroborate the company’s claim. Business owners can see a full list of WePay’s “Prohibited Activities” here. If your payment platform deals with one of these industries or is similar to one of the business types on this list, be aware that you may be subject to the sudden cancellation of your account even after fully completing the account setup process.

Our WePay Review Summary

Our Final Thoughts

WePay currently rates as an average credit card payment processing provider. On the surface, the company offers transparent rates without hidden fees, appealing to many business owners. However, its stringent fraud prevention measures and prohibited activities policies have sparked numerous WePay complaints. Similar to Square, WePay initially attracts clients with its user-friendly terms, but its overall rating suffers due to poorly communicated fraud prevention policies and inadequate customer support.

Developers operating in online marketplaces might find WePay suitable for their online payment processing needs. However, it’s crucial for all users to ensure their business type isn’t prohibited by WePay before setting up an account. This proactive step will minimize potential disruptions and help avoid issues with fraud detection or customer support later on.

Location & Ownership

WePay’s headquarters are located at 3223 Hanover St. Palo Alto, CA 94304. The company’s CEO is Bill Clerico.

If you found this article helpful, please share it!

In the late 2000s, as a broke college student struggling to make ends meet, I was contacted by a merchant services company after uploading my resume to a job listings website. This company promised substantial commissions and ongoing residual income for simply persuading businesses to accept credit card payments. It seemed straightforward enough—after all, what business doesn’t need to process credit card payments? Following a phone interview with a persuasive “sales director,” I found myself embarking on what I believed would be an easy job that would significantly boost my bank account with reliable monthly income and large sales commissions. However, the lessons I learned would profoundly change my life in ways I could never have imagined.

After completing my sales training, I hit the ground running, eager to make sales. This broke college student was determined to improve his financial situation! My first attempt at a cold call, with no prior appointment, ended with a burly man in his 50s yelling at me to leave, claiming he had been “totally robbed” by someone like me before. As I hastily exited, puzzled and intimidated by his reaction, I couldn’t help but wonder what he meant. Throughout the day, I encountered similar hostility from other business owners, all expressing disdain for the industry I had been so excited to join that morning. Confused and curious, I decided to shift my approach from selling to listening.

I quickly uncovered that the merchant services sector was riddled with unethical practices, including hidden fees, deceptive marketing, fine-print traps, and much more. It dawned on me that I had nearly been tricked by a dubious company into selling overpriced services under contracts with long-term commitments, all without being fully aware of what I was promoting. Outraged, I resigned from that company but learned that there were indeed ethical credit card processing companies that treated their clients fairly. Over the next four years, I worked for one such company, assisting hundreds of businesses in securing cost-effective processing solutions. Yet, I also met many more who had been misled and trapped in onerous service agreements. Determined to help people steer clear of these unscrupulous providers, I launched this website in my spare time, dedicating myself to researching and sharing my findings on every merchant account provider I could investigate.

Gradually, more and more business owners began to discover my articles. As word spread, search engines started to rank my content highly, amplifying its reach. My efforts were making a difference! Eventually, the website garnered enough traffic to enable me to leave my job and focus on it full-time, a journey that has now spanned over a decade. This path has not been without its challenges; unscrupulous company owners have tried to intimidate and sue me into silence on several occasions. Yet, I have stood firm against each threat. Here I am, continuing to publish reviews and articles, hoping to safeguard others from the pitfalls of the credit card processing industry.

If you believe in my mission and wish to contribute, please share my articles on your websites and social media. Thank you for visiting!

Testimonials & Complaints

How Did WePay Treat You?

341 User Reviews

Alex Kearson

Omega Environmental

WePay will take your legitimate, everyday business transactions for no reason. They will hold the funds from your business account under the pretense of reviewing the transactions. This has happened to my business more than once when WePAy was used.

I watched a video of Warren Buffet speaking about this practice. Warren Buffet says that the banking system calls these “float accounts,” where they hold your money in these accounts for no reason other than to accumulate interest at your expense. WePAy has done this to my business twice now.

Paul

What an absolutely awful company!!!!!!! I spent several hours on the phone interview process and carefully explained our business and the transactions our business would be conducting. On April 15, 2024 we processed a $1 test claim which successfully transacted. Our first real transaction was on April 29 and our 2nd transaction was on April 30. I noticed on April 30th that the transaction from the previous day was in a “hold” type status, however, i did not pay too much attn to it. On May 1st, i logged back in and noticed that neither of the transactions had completed and that payment had still not been released for either transaction. On May 2nd, i started receiving emails that there was a problem with my account and that the funds for both transactions would be held for 120 days plus. The next email that followed the funds hold was that the account had been closed. The 2 transactions that we processed were completely within the parameters of what had been discussed during the interview process. Let me be very clear to anyone reading this……There is no one to speak to at this company. They hide behind a status of “we dont have a phone contact support network”.

I would highly recommend looking elsewhere for a payment processing company. I am extremely disappointed with Chase as i really thought that they were a better company than this.

Fortunately for us, we were using this company as a test pilot, which is why we had only processed a couple of claims. I have reached out to of one my customers and asked them to dispute the claim and that 1 claim has been paid via other methods….the 2nd claim i have left in their queue just so that i can follow up with the Attorney General in 120 days.

Ron Spangler

LRS LLC

Unfortunately I have had to resort to coming here and placing a complaint against this company. I am a small restoration company that has accepted only two other credit card payments ever and they chose not to honor a payment made to me by one of my customers for almost $20k! Their only explanation, which of course was received via email, was that my account was susceptible to back charges(which I’ve never had) and discrepancies that they could not elaborate on. They have now closed my account yet are keeping the funds ($20,000) for 120 days….120 Days! This is absolutely unacceptable. If my account is closed then there is no reason to keep the funds as they have no vested interest in my company or it’s financials at this point. I owe them NOTHING! With the amount of complaints just here alone, I think it is safe to say they are withholding monies on a pretty regular basis, which should be unlawful and unethical. My customer is now going to default with their own insurance company because repairs that are required within the allotted permit time will not take place. These practices have a trickling affect on more than just my business. Obviously WePay has their own agenda and that does not include helping their customers. I’m sure they’re banking on the interest of hundreds of small business owners as we struggle to pay our employees and keep our doors open, all because they want to play games and hold our money for an unreasonable amount of time! I will be escalating my complaint against this company to my State Representatives, Attorney General, FTC, the National White Collar Crime Center (NW3C) and the Payment Card Industry Security Standards Council. I would advise anyone else that has been the victim of this type of procedure to do the same! My livelihood is in the balance here as I am unable to complete the contracted work I am committed to because of this incident. I just want the money my customer paid me!

Anthony Rose

Golden State Technical Solutions

Wepay is a scam and stole my money and shut down my account without notice for no reason at all and refuses to answer their email.

Andrew

I can not overstate this, stay away.

We process incoming and outgoing payments through Buildertrend which uses WePay as the processor.

Nearly 100% of our payees have had issues where WePay shut down their account without notice and froze their funds.

Each time we reached out to Buildertrend (WePay is unreachable) they were told by their internal communication with WePay that WePay cannot give any information and it cannot be appealed.

Keep in mind that we are not just a valid corporation with state licensing, we only send out payments to companies who we have verified their LLC listing and their licensing (electrical, plumbing etc)

These are not handyman style companies with shady backends or depositing into personal accounts etc.

We have been told by Buildertrend which is a reputable multibillion dollar company that the issues have gotten so bad with WePay that they have been forced to develop their own payment processing system.

Kevin

K&S

You are 100% right STAYAWAY. IN A 2week time period they held all my customers verified payments,returned payments that were not disputed,now holding all funds for 120 days ,closed my account. I can email only an appeal and there is no one to call. Digusting, if you or I did this our businesses would be shut down and we would be in jail.

Claudia J Sheets

Sheets Floor and Design / Sheets Floor Covering

We had the same experience with wepay, We are a small buisness, we have been in business since 1979. we have a good credit rating and have alot of return clients for years. Wepay held $7100.00 for 120 days with no explanation. This happened after my husband bei ng off work for 8 months after open heart surgery. This was the worst thing to happen. I sent letter after letter, phone call after phone call…they are legally using their clients money, charging a fee and collecting interest. They need to be held accountable. They are the worst for small businesses. I wish that someone would get a class action lawsuit going. I hope soon…

Hans

WOLFdens US, LLC

Stay away from Wepay. My customer wanted to pay over the internet and Chase Integrated Services uses Wepay. The funds went in and Wepay put them “In Review” with no explanation. There is zero way to contact them other than by email. Chase business cannot help you, they cannot even contact WePay upper support. My Business Relations manager, my bank Manager, noone can contact them. When it happened 2 days ago, they had instant chat available on the help site. As of today, all links to live chat have been removed from their site.

I will now be completely changing my processing as this company is atrocious.

Hans

WOLFdens US, LLC

Update: Wepay sent me an email that they cancelled the payment as I need to “verify my information prior to accepting payments”.

I had already verified my information with them. Secondly, they are a JP Morgan Chase company and my business accounts are with Chase with all information verified.

Again, I cannot recommend strongly enough that you should completely avoid any business activity with Wepay.

Quality pros paint plus LLC

Quality pros paint plus LLC

WePay is a scam

They want to gat the money from my clients

And don’t release it they hold the money and put to many tricks to don’t release it

I’m totally disgusted with wepay. They take my clients money instantly. They show me on the app everything is going great. when it’s time to release the money. no money, they say someone would contact me in 3 to 5 business days. then I get email that account is closed due to high risk and they still have the people money and now want to hold it for 120 days pending what? They have the people money. this kind of practice is definitely criminal on the lowest level. I’m truly truly ashamed for wepay if they don’t care because it’s clearly apparent.

Kiley Williams

Kilwil construction inc

I’m totally disgusted with wepay. They take my clients money instantly. They show me on the app everything is going great. when it’s time to release the money. no money, they say someone would contact me in 3 to 5 business days. then I get email that account is closed due to high risk and they still have the people money and now want to hold it for 120 days pending what? They have the people money. this kind of practice is definitely criminal on the lowest level. I’m truly truly ashamed for wepay if they don’t care because it’s clearly apparent.

Shawn

Stay away. They will hold your funds with no explanation. Your only option is to email with no live customer support. 2/2023 the are holding 10 for over a week and no one has an explanation.

Farmer

FMHERS

Worst processer around, cant call them, only email. I recently started a company as an S-Corp LLC. Well they say its a corporation & i need to select the appropriate box for corporation even after sending them the info letting them know its not a corporation that its an LLC. I even sent them multiple emails & get the same response, which is garbage. Ive even requested a paper check multiple times as theyve been holding my money for 2 weeks now over some stupid bs. Im going to post this 1 star review everywhere i can.

Julius Jones-Carter

I run a small contracting side business. I use the freshbooks application to keep track of expenses and to bill clients.

Recently a client wanted to issue a Visa payment and through Freshbooks I opted to use WePay as the payment processor.

Freshbooks collected all the necessary information for verification in order for my clients payment to be processed.

Once the payment was processed it was added to my WePay Balance (same day), no holds, no pending status, payment was accepted.

I have been receiving ‘failed settlement’ emails for three days now.

WePay has all of the information necessary to release my clients payment to my bank account, yet they refuse to release it, sending me a notification email with no information regarding why the settlement has failed.

After contacting customer support (who you can only communicate via email btw), the agent gave me a set of verification instructions that were literally impossible to complete because their User Interface has no links available to upload additional documentation.

After a frustrating string of back and forth emails where the agent repeated a set of instructions that were impossible to meet, they indicated that my account was being reviewed by their Trust & Safety Team.

The Trust & Safety Team has not reached out to me for additional documentation and why would they? They already have the information uploaded to Freshbooks during the registration process.

So now, my clients payment settlement has been declined three days in a row, without being contacted by a team that is apparently withholding the funds in an account I cannot withdraw from.

This Payment Processing Company takes 2.9% + $0.3, has a support phone line that directs users to an email support line, is terrible at responding to inquiries in a timely manner and has a limited user interface.

After this transaction is settled (who knows when that will be at this point), I am never using WePay as a payment processor for my small business ever again.

Cecy

This company Wepay used the name Hiedi Jones and charged my father who is on a fixed income over 600.00 between 10/05/2021 and 10/06/2021. Under product they used “Donation”. Wow! Freaken thieves.

Alex Morton

Junk Star Handcrafted Furniture

Unless you want to HATE an inanimate object stay clear of this merchant service company. They NEVER deposit consistently, they settle when they feel like it snd they have no human customer service to speak to. They are unpredictable and unprofessional. Their excuse is that their Safety and Trust team is doing a routine review for your safety. Lol! More like floating money!!! They take money from the clients and don’t deposit until they feel like it. No uniform proceeding. Like I said, they will make you HATE them. They have no concerns for the business that are their clients and I totally predict them going out of business. I spoke with Chase integrated service about it snd they said although they are told to recommend and sign companies up with them they refuse to because either the companies leave because of unpredictable deposits or Wepay drops them for no reason. He told me he is sick of getting all the complaints and We Pay never takes on their own issues. The only way to reach customer service is to email and they won’t respond to even that. Horrible business!!! STAY CLEAR! If you don’t believe me just go to the BBB and look them up! It’s crazy!!

Jason

Jasons painting

Holding a small $400 dollar payment asking all sorts of questions about my work and reviews for my company. I’m not working for you, you work for me! JasonLook it up for yourself! Closing amount and leaving chase business checking.

Vanessa Barrera

https://order.diemtheapp.com/

I’ve been waiting for my payment that I worked for. They said it would take 1-3 business days and still haven’t recieved anything they are like Indian people they have tat accent.

Kelly Davis

WePay has been withholding a payment we received for over 2 weeks. They are inventing false reasons to do this. Please stay away. They are a total scam.

Aaron Davis

They constantly hold my money for extended periods and are entirely unapologetic about it. They want us to verify our bank account repeatedly (that’s their excuse for hold my money.)

The only reason I use them is because of an integration with my crm. But that slight convenience is now being outweighed by their complete disregard for my business cash flow.

Timothy E Brummer

Lost $8000 because Wepay are worthless crooks.

They don’t care if customer lies about unauthorized charge.

We shipped to valid billing address and obtained valid signature.

There are several reasons I am dissatisfied. 1-I opened this account a while ago before I had clients and when I ran my first transaction after two days of waiting for the money I was advised that you couldn’t work with me. It would have been nice to know before I ran a transaction as I opened the account one month before the first transaction. 2-It took a REALLY long time to get a response from support, over a week! There is no phone number to call either. 3-Support was unable to give me a reason you couldn’t run my transactions or work with me.

David Edwards

WePay derails MealTrain

WePay handles the funds for MealTrain accounts. Of course, when I say “handle”, I mean steal – at least in my experience. I have spent HOURS trying to track down $27 that was donated to my wife and me when we had our child almost 5 years ago. WePay has only made this process more difficult and we have yet to receive the money. TERRIBLE service. Just terrible. Avoid this company like the plague. You have my sympathy if you have no other choice – as was the case with us.

Roger Bryan

STAY AWAY – They will cost you money!

If you value your business I would stay away from WePay. In 13 years of business I’ve had three change backs. The first two I provided the same documentation I always do with proof of service delivery and won my case. We switched to WePay (via Freshbooks) in early 2019 and had one charge back with them. Then came the issues:

1- Their charge back system has file size limits that don’t allow you to submit all of your documentation.

2- They don’t read your notes section in their system when you submit your documents (where we said we had 47 pages of of proof of delivery).

3- They don’t respond to your requests to provide the additional documentation

4- They say you lost your defense because you didn’t provide proof of service delivery

5- When you email them to point out their lapse of care for their customer they tell you “I know this can be frustrating but our system doesn’t allow you to provide the documentation we tell you that you need to provide, so sorry but you’re out of luck.”

You can do everything exactly right, exactly what your attorney tells you to do, everything that works in all other cases, and WePay doesn’t care. I would go as far to say they have a breach of obligation in their processing of charge back defenses.

Stay away from this company. They don’t care and are negligent in their operations.

Thor Tufte

Wepay sent us this email yesterday..

“Upon review, we have determined that we will no longer be able to process payments for your WePay Payments account. All pending payments have been canceled and any existing payments will be refunded to the payers.”

I filed a ticket requesting to know the reason and received this..

“Regrettably, we are no longer able to process payments for your account. Our banks and processors hold us to a strict guideline on what we can and cannot process through our site. As this information is proprietary, we will not be able to offer more information about these guidelines.

We wish you and your efforts the best, going forward.

Best wishes,

Mira”

We are in retail selling handcrafted Italian leather bags. I guess that’s now prohibited, banned by Wepay. I’m going to follow up and see how long it takes for Wepay to process the refund. A real payment gateway (even Stripe) would flag a transaction suspicious, but not close the account without any warning. Wepay accepted all our documentation in order to open the account, and now it gets closed without any explanation. If Wepay is not a scam it is as close as you can get without crossing the line. Don’t touch this business, not even with a 20 ft pole.

Kyle

Stripe isn’t a real processor and in actually is the same as WePay and yes they do the same as WePay but instead of refunds they hold the funds for 6 months. They aren’t ones who hold the merchant account. Not you.

Kamel Toubache

Hello, I created a campaign using GoFundMe and have had already 2 donations cancelled. WePay appears to be responsible for money matters. The reasons for the cancellations are not convincing. As you indicated their customer service is very poor. It is slow and appears at times mechanical (repeating what was said in previous messages without addressing additional questions). Also, it is a struggle to have them pay back the donors after they cancelled their payments. I am considering cancelling my GoFundMe campaign if that continues.

Thanks for your good work.

Kamel

Rorie Burke

DO NOT USE WEPAY! The absolute worst! No customer service line. it’s all done by emails. they explain nothing and they can refuse you service on any sort of basis, and then not explain why. The worst online company I’ve ever dealt with. They waited to tell us they wouldn’t work with us until we had a large check in their system. Been fighting to get it ever since….

Mary

WePay is horrible. We signed up as a new customer. We have been in business for 11 years but wanted to try a new invoicing system. To continue to allow our customers to pay online, WePay was one of the merchant services that was integrated with the system we chose. We decided to try it. Our very first invoice, a payment was made from a client of ours in excess of 2k. WePay took the payment form my clients AMEX. I received the notification I was paid. It all looked to be fine. But here is the kicker…they haven’t released my funds to my linked bank account. So they have my clients money, took their fee and will not release to me.

There is no way to contact them outside of “support” tickets which they do not answer timely or at all.

Finally got to the “review department” and they sent me an email asking these questions:

• What services or products do you provide? Please be specific.

• How do your customers find you?

• What’s your website and do you have any online reviews (think Yelp or LinkedIn), please provide the links?

• Are you a sole proprietor or LLC?

• If applicable to your business, please provide copies of the following: licenses, permits, surety bonds, insurance documentation.

• If you have registered your business with Secretary of State, could you send documentation of your filing?

• Do you have any paperwork from the IRS about your incorporation (for example, registration of your EIN number), if yes, please provide a copy?

• How much payment volume do you anticipate on a monthly basis?

Now I am all about security, but I already had to verify my identity with my SSN. And I feel this should have been part of the set up process not after they collected money and hold it.

I cooperated and sent them my State Articles of Organization and well as my EIN and my licenses etc. They are still holding my funds and haven’t even responded.

This appears to be a scam. I have written a letter to the Acquiring Bank- Chase, who I am a BUSINESS customer off to inform them of this. Sent via fax to the Executive office. We will see what happens. I am doing all my due diligence before lawyers gets involved.

At this point, it is really nothing short of theft/fraud. I will give them 2 more days to release my funds. Then we will escalate this matter.

WePay is demonstrates extreme unfair business practices. They continue to hold funds that have cleared and even after the fee is collected. Basically they pay themselves and keep your money. Horrible customer service. They do not respond to “support” tickets yet there is no other avenue to contact them.

If you are looking for merchant services, Run from WePay. They are thieves. I have reported them to the BBB and plan to file a suit against them.

We had integrated WePay with our Zoho books and after a client paid, the process to get paid has taken over two weeks. They did everything possible to hold on to over $4000. When I asked about this they blamed Zoho books and then offered to helped with a request for six months of my transactions for to get one transaction. I cancelled their service. Don’t waste your time with this company if you are small business.

Wepay is awful, do not use, it should be called wedontpay they held a large sum of money for over a month without notifying me anything!!! i had to do all communication through freshbooks, no phone number. when i was finally able to email with them they were rude !! and did not resolve the problem. eventually refunding my buyer for merchandise he had already for 22 months.

I am a customer of a handyman contractor who paid him through Joist for $748 worth of work. My bank account was solid. He was threatened with having his account cancelled and my bank account left the transactiin on “processing” followed by the transaction simply disappearing from my statement. No communication to date has been made to me by either my bank or Chase bank or Joist or WePay explaining what has happened with this ghosted transaction since June 28. Now it is July 6.

Count me in. This company is terrible. At the very least I will be reporting their behavior to the BBB and recommending to the platform I work with that they discontinue their relationship with this company.

Daniel Chatzaras

Absolutely a horrible experience!!I had over $900 dollars deposited into my account by my employer. When I went to get it out they said that I had a secondary account, which I do not. They also claim my account was negative $2500.00! I have never used this company for any other reason but to collect my paycheck from my employer! I have no idea what this is about. There is no phone number to contact them! No one has contacted me to explain this! This is robbery with Chase’s bank name associated with it. I just don’t know what to do!!

I made a mistake in opening a Wepay account. I own 5 cell phone stores. The business has been opened over 15 years. Not a new business at all. I needed a new platform to receive payments because I wanted to differentiate between different business’ incomes and I found Wepay through Zoho books.

Now, Wepay states that you will get your money in 2 days. That is a big marketing lie. I received my first payment-not a big payment, but just $1640.00-and I was out of my money for over 3 weeks.

When I contacted Wepay, they asked for all kinds of statements and documentation, to assess if my business (retail) was a risky one. I sent the asked credit card and bank statements, thinking these documents may convince Wepay, of the business low risk, knowing that it has a very low chargeback rate(lower than 1%). On the contrary, Wepay declared the business high risk, by their policies.

I’ve been in business for a long time, and I have used, and presently use, different platforms, to pay and receive payments, and I can confidently say that my experience with Wepay is the worst I have ever had with providers of this kind of services.

I donated $20.00 to: Get Zo to Spoken Word Nationals in Vegas on May 30, 2019.

Wepay charged me $20.00 three seperate times on that day, $60.00 total!

I’ve emailed and have gone through their ’email’ process complaint.

I just want my $40.00 back that they overcharged me.

This is it for me. I’ve helped people through gofundme before. Never again. It’s a shame one bad apple has to spoil it for everyone.

Siobhan

DO NOT go with wepay use STRIPE instead. Wepay refunded £1000 worth of goods unnecessarily of a friend of mine and this week, WePay closed down my account WITHOUT notice WITHOUT an email or message. The account doesn’t even have an error message on it…even though they have an alerts section on the portal.

Both myself and my friend are small business’ and it cost her £1000 in produce she could not get back and it has cost me nearly £850 of developer fees to try and find the issue AND cost me the launch of a new online product campaign.

Their response time is ridiculous, I waited 36 hours for the first response, and on average 16-20 hours each time. They screwed up YET again when I did what they asked, and now I have to wait 3-5 business working days to get the account active.

I am closing my account and going to Stripe.

Also, they don’t have a direct complaints department.

I have never written a bad review ever, but I am appalled by their system, processes, response time and attitude when it is their error.

1st time I’ve ever left a bad review, that’s how ridiculous my situation was handled by WePay. I’ve processed many payments totalling thousands of dollars via check and credit card via BuilderTrend who uses WePay. Never had a single problem or issue with any transaction.

Today I get an email out of nowhere claiming that they can no longer offer me service because my company was determined to be at high risk for chargebacks and/or disputes. Interesting, considering our perfect history with them. Then, they inform me in a separate email that over 40k in pending payments are being refunded to customers. No sort of heads up, just have a nice day and good luck dealing with it.

Scramble around trying to find a number to call, has to be something that can be cleared up easily right?? No chance. No phone number, no dedicated email address, only option is ‘submit a ticket’. And then the BS response you get is obviously a templated response they send to everyone.

Amazing that companies are able to operate in this manner and get away with it.

Horrible, I’ve been am active user of the app and website Joist for years. Joist used to collect and process credit card transactions but this apparently now has been taken over by WePay.

So, as a legitimate company (LLC that’s been in good standing since formed in 2011) that has been utilizing this set up to invoice and collect payments for years with my linked business checking account with one of the largest US banks, I have a large corporate customer make a payment for $2500 and get an email from WePay asking for verification documents ( W9, LLC info etc ), that I promptly provide and after a couple hours was told they consider my business a high risk for chargebacks, and that they are refunding my customer and disabling my account.

Now, I’ve NEVER had a chargeback, OR ANY PROBLEMS EVER, so now my customer has to contact the company they use to issue payments and track all this down, this makes me look completely unprofessional, and it won’t even let me log into WePay anymore to see the status of my current account and money owed to me.

Also of note, I spent hours on the phone with Chase being incorrectly transferred to different departments since no one there has basically even heard of CHASE WEPAY, only to get disconnected.

Worst possible experience I could fathom, basically makes me want to close my personal banking accounts with Chase as well just for being associated with this crap.

Wepay is the worst! They hold you money way too long for no reason and they’re idiots.

They cant even perform the simplest of customer service problems…probably why they dont have a phone number because they’d be getting yelled at continuously by unhappy clients. Literally use any company other than wepay!!!

Should be called “WeDontPay”. As my business grows, so do the deposits I collect up front from my clients on big jobs. Given, it was a large transaction, but WePay was incredibly unresponsive after they notified me that the transaction was being held in review. I sent them many, albeit frantic messages, and they would review them and not respond. Ultimately, they notified me that the transaction was being cancelled, but now $20,000 has been released to them from AmEx, and this rush job has come to a screeching halt. Go with Square. If you’re trying to grow your business, avoid these guys. Would’ve helped if they has customer service, or support or anything other than a ticketing system where they don’t respond!

WePay has the worst customer service of any credit card processor I have EVER used.

I use Square they are great and 3 other vendor.

WePay is by far the least helpful and their back end is definitely NOT for the user. They have no one to call for help. Now they are redirecting emails!

How illogical is it that I can’t search by the customers name?

Unfortunately, I am stuck with them on one of the platforms I use for my business as that is the processor they use.

If you have a choice, I recommend NPC, Square, or just about any other than WePay. I had a chargeback and proved my case and they would do nothing.

They wait until they have a substantial amount of tour money and then put a hold on it. They will ask for a whole laundry list of dubious info about your business. If they want the info they should ask during account setup. My opinion is this is a scam

Over 15 years in business and customers are under contract. Tried Joist for quickbooks integration

Here are some of their questions they want answered before they will release your money

Clear description of the work being done

The relationship between the payer and the service address

Can you please review your invoice, add any missing information listed above, and then attach the updated invoice in your next reply to this email?

Additionally, we do have a few questions about your account. We’ve had to pause your payouts for now, but as soon as we get the information requested below we can start them right back up again.

What services or products do you provide? Please be specific.

How far do you typically travel for work? What is your general service range?

How do your customers find out about you (e.g. online advertising, word of mouth, flyers, etc.)?

Do you have any online reviews (Facebook, Yelp, etc) for your business? If so can you provide the links?

Can you provide supporting documents from the below list (as many as possible) related to your business? Simply take a photo of any document you have with your phone and include it in this reply.

Contracting license or insurance.

Articles of incorporation.

Business tax documents.

Registration with the Secretary of State.

What’s the total dollar amount of credit card payments you plan to receive through Joist every month? Please provide your best estimate.

As you can see, some of this is very suspicious. That they wait until they have your money to require this info is very concerning

WePay is a decent processor until your business starts making decent (the point of a business) and they start holding all your funds for a “reserve limit”. To up your limit they require you send them 3-6 months of bank statements. When I FINALLY got them to raise my limit after a week of dealing with AWFUL customer support, they only raised it by $250! I have thousands just sitting in WePay since I can only actually take out 1.25k/week.

Now i’m having to have all my clients fill out new payment info so I can switch to Stripe.

Horrible. Found a withdrawl on my account from wepay. I have no idea what it is and cannot get anyone to answer my questions about it. There is no customer service and the website is no help what so ever.

They cancelled the payment my client made to me with no explanation. They originally asked for me to provide more detailed documentation regarding the service I was providing to my client as part of their risk assesment, so I sent over my contract as well as my very detailed and lengthy proposal. I do fashion and beauty brand consulting, there’s nothing risky or out of the ordinary, or anything that goes against their terms of use. If they had even looked at my documentation they would see this. But they did not and just cancelled and refunded back to my client without further communication as to the reason for the cancellation. Not only that the refund process takes 3-7 business days and I have already sent properietary course modules to my client and we have a kickoff call scheduled in a couple of days, which we’ll have to push back because of this ordeal. This is the worst payment processing experience I’ve ever had. I’ve always used PayPal without a hitch and they transfer funds within one business days. Canceling my payment from my client without any explanation or any review of my supporting documents (which they asked for!!) is completely unprofessional and has now caused me and my client much stress and time wasted. I will never use this company again and I advise you to stay away.

A client of mine just made a deposit over the weekend and by today, as of Monday, they emailed me without warning and said I was at high-risk for charge backs. I just opened the account and new to my business. 4 total transactions made since I opened, zero charge backs. My client made a down payment of several thousands and I assume that alarmed them so they said I was due to high-risk and immediately closed my account. They sent my clients funds back. As a new business owner, I need the funds to operate and create more business. I lost a ~$6,000 job because how embarrassing it was to call my client and tell them, something went wrong with my processor. If I had known this would of happened, I would of processed with someone else from the get. If the money gets charged back, I will pay you my self. But it doesn’t because I ensure contracts and loyal service to my clients. Now I’m offline for online credit cards until I can get another one. I should of known from beginning since it’s a chase company. Don’t forget about the year it takes to get to your account. 0/10. I wouldn’t recommend this service to my dead relatives.

I have had nothing but a headache 1st of all i am a small new business owner i singed up with homeadvisor who in return said i needed to sign up with mhelpdesk in order to recieve credit card payments so i took there advice and signed up at 50+$ a month so i did my first credit card payment through the homeadvisor pro app and filled out my invoice through mhelpdesk now here is where it get sketchy i was under the impression that mhelpdesk was responsible for my echecks and credit cards come to find out they use wepay. Now when i ran the credit card i ran it under the customer name not realizing her significant other had paid for it i get that so the next day i recieved a email from jack stating that wepay needed more information such as the correct name on the credit card his address relationship to the customer and a in detail of the services that was done so went back to mhelpdesk and had a lady to walk me through this process as i said im new to this so as i said i had a lady from mhelpdesk help me with the invoice and all the correct information before resending the invoice to wepay once all the information jack requested the invoice was sent to jack then the very next day i recieved another email saying action required so i tried to get in touch with wepay at support@wepay only to find out its a wrong address so the fowlling morning i received a email from peter stating he needed more information whis is the same as before so this time i called mhelpdesk and spoke with mike p and he went over the invoice to make sure everything check out and it did so he himself emailed the invoice to wepay as so did i i copied and pasted it to the direct email then this morning i get another email stating action required so now im up to sending 5 invoices have trie on numerous occasions to get in touch with wepay i did find out they dont except direct emails so now lets go down the list no phone number to call wrong web address and no direct emails that a whole lot of skepticism at least with my old company i could call and get a pre approval and talk with a live person i went with this company because it had a lower fee but what im reading on here is they just take what they want and give you your money since i had to put my money up for the initial job and i haven’t received payment from wepay my company has been shut down for three day now and will be lucky if i still have a business come monday so much for there business platform of helping the small business owner yea they helped helping put me out of business i wish i had done my homework and researched it better on there website i read some reviews but now i understand they only picked the good reviews to put on there after doing my reserch lead me to this complaint form so my advice if you hear the name wepay or mhelpdesk run or be ready for nothing but a headache o did i mention they took there fees the 1st day im on day 6 no pay

We started to use this processor for a small business. After being connected and up and running for two weeks, they abruptly stopped our account. After no communication for days, they said we were “high risk”. If I had known prior to, I would not have taken peoples payments.

WePay- please help improve your customer service. I know you dont care about small accounts, but it hurts our business.

WePay does not have a phone number, just email. They closed our account without giving any thought because the amount was getting bigger and they could not access our protected site. Seriously bad support. Now they are holding over $15,000 of our money for 60 more days. WTF. They don’t even make an attempt to satisfy their customers.

I highly recommend against them as they might damage your relationship and reputation you have with your customers and cost you time and money. We are an established business representing the estate of a rather famous artist from the UK. We’ve been selling art related products over the last few years without issue. In fact, after several hundred orders we’ve had no issues with payments or complaints with Stripe or SquareUp and just one dispute with Paypal, (a damaged item received which we resolved).

Then WePay showed up! We added WePay through our Ecwid store and an order came through for $231.99, our first and only order with WePay. Two days later I received an email stating:

“Unfortunately, we can no longer support your business and we’ll need to cancel any pending payments.”

And they canceled the order in our store!! It happened without our knowing and I have no idea what the customer thinks yet but it doesn’t make us look very reputable because, WePay IS NOT reputable.

Why was this? Because they decided that our “account is susceptible to a high chargeback or dispute rate.” However, if we only had this one sale, no other activity, no chargebacks, no disputes, nothing, and a track record of success with our payments, then this decision is unsubstantiated.

Many others have similar complaints and if the WePay response is true, that their “processor holds them to high standards and has rules regarding accounts that are seen as high-risk” THEN WHY DID THEY APPROVE US TO BEGIN WITH?

Also, I reached out to Ecwid support and ‘Alex F’ said; “That sounds pretty strange in this case. Possibly, if you contact them and ask to reconsider their decision, they will reopen your account.”

Reconsider? After this, why would we ever want to do business with such an untrustworthy company like WePay? If we lose this sale or our reputation is damaged, I’m filing formal grievances with the BBB and anywhere else possible.

Lastly, I strongly advise against anyone using WePay, if you read the reviews/complaints they have a consistent track record of holding money hostage and damaging a businesses reputation.

This is the worst CC processing company I’ve ever seen. We have a chargeback that still shows open that’s over 120 days old. Ask WePay where it’s at?? Nothing. Try calling them? No phone number available. They had no issue pulling the money from our account immediately. And they had no issue overcharging fee’s on transactions…

I do enough with Chase (who now owns WePay) to move up their chain to get to someone high enough that has a contact with WePay, and even they said it was a mess at WePay. Terrible, mismanages series from internal communication, and emails being sent to the wrong people.

Do not use them for anything whatsoever. And if you use FreshBooks, don’t let them talk you into it.

I’ve found the WePay did not submit our data in one chargeback as well. So of course, we wound up losing the charge with Amex (which we’ve previously won 100% of the time with our previous CC processing company).

Go to a company you can speak with. If you’re considering them, look for a phone number and try to get ahold of them. Consider if someone tries to scam you, and they won’t support your dispute with the CC company, and how much you’ll lose.

I’d honestly rather deal with Comcast or Blizzard support. I’d rather go wait in line at an apple iPhone launch event in search fo a Samsung phone.

I can’t convey how much I despise this company and that terrible / shady “cost savings” tactics the implement.

I recently signed up with wepay because they advertised a one day to 2 day processing time. My first 2 charges were paid in a timely manner. Only after I started getting more charges they stopped releasing my funds to me without any notification. After reaching out to them inquire why they said it was to protect me from chargebacks and will hold my money for up to 10 days.

After numerous emails, the company has refused to pay me my funds so I must wait 10 days to receive my funds during the busiest time of the year for us

Oh my gosh, I think I will close my bank account as soon as they refund my account for the $635 invalid charge. I am complaining as a consumer who was trying to purchase a product. WePay properly billed my account for the real purchase $211, but they turned around two days later and charged me another $635. Their link for ‘unrecognized charge’ says there are no transactions for my card number or my email address! Their auto system has the gall to say that I mistyped my own card number (last 4)! I will reverse the charge but will also file a complaint with the FTC and my state’s attorney general tomorrow. Btw, the product I was purchasing was for an autoimmune disorder. STRESS is the number 1 no-no. After having my bank account cleaned out, I would say that my stress level is really high. WePay doesn’t even have an auto-reply when you send them an email and judging by the complaints here, I don’t expect any response. We will see. bad, bad company, can’t believe they are business, and that they are tied to charitable fundraising. I won’t ever give to gofundme again and youcaring as it is clear they are tied to WePay.

Robin Hall

We processed our payments through WePay for around 4-5 years. In the beginning, there were never any issues and no delays with payments. They processed overnight and were in our bank account the following day. There were 2-3 occasions when there were processing hiccups on their end that caused a delay and it took 2 days for the deposit to post to our account. In the past 12 months, we’ve experienced more and more delays. There is never a notification to the merchant of the delay, so if you are anticipating the deposit posting the following day, you may be in for a surprise when it is not. You should always be prepared to cover outstanding drafts on the account as their service is becoming more and more unreliable. When we ask about the reason for the delays – some taking upwards of a week (6 days) to process, we are simply given blanket canned text responses of “the delay is on our bank’s end” and that “there were a few engineering issues that are being worked out” and that we should “wait 2 to 5 business days for monies to post” and that they are “not responsible for delays by the merchants bank”. When we contact our bank, they have no record of any incoming deposit transactions. Generally after the email (you have to email, because they refuse to release a customer service number to call), the deposits show up in the account within 1-2 days. The service is unreliable at best at this point and we have elected to take our business elsewhere. We can’t run our business not knowing when we can expect deposits. I would not recommend WePay to any merchant and we will never use them or their partner Freshbooks again.

I was looking to start up with WePay but after so many negative reviews, I’ll take my business elsewhere. I can’t wait 6 days for payments to be returned. No excuse on your part, sorry, the engineering issues coming from a person in IT myself, don’t buy it. Get yours tuff together.

I could not agree with this review more! The exact thing is happening to us and it is beyond stressful.

Today is 11/28 and I’m still waiting for deposits from Thanksgiving to arrive.

Getting a canned response is unacceptable. No one even bothered to look at our account which was obvious from the generic reply. Just some goober sitting behind a computer buying WePay another 5 days.

Shockingly Shot – I will let the reader guess what vowel I changed.

Signed up for WePay – thought we would give them a go. Spent two hours signing up for their nonsense service, then another half hour making a test purchase of £10, then had to wait another five days for them to process it, only for them to shut the account saying high value transactions aren’t available! Wow! No joke!

They then said they would not allow us to close our account in case they want to take money out of our bank for the single £10 transaction that we made.

Honestly I would avoid this company and service at all costs.

This is a very difficult company to work with. Very slow customer support turn around and they hold your funds until you do exactly as they say – upload files (although no easy path to upload), provide member data. I don’t remember being more frustrated with a financial services company (save maybe CapitalOne)

Payment by my client was on a Weds, after 4:00pm, it is Saturday, mid day, and i had to pay $32.00 for this?

3 reps told me 3 different stories, WePay tried to BS me.

Bottom line is I would love my fee back from this rip off service!

Worst Merchant I’ve worked with. I received 4 chargebacks from a client who just decided to stop paying for a program. We submitted emails, signed contracts etc… to prove the charges were legit. We won. Then two months later the same client charged back the same four transactions (that we already proved were legit) and won but they had already refunded the money back to them and so we were out the four payments plus fees on a dispute we won.

Now they are holding a large amount of money from me without prior notice.

The deposits take anywhere from 3 – 7 days to hit my account as well.

These are just three of the many issues we’ve had with this merchant.

We are looking for a new one and will transition within the next few weeks. I can’t believe they are still in business.

These people are a bunch of thieves do not use them they will put a freeze on your money and make interest on it while they insult you and hang up the phone on you

We have never heard of this company until we had an unauthorized charge of $400 on our debit card at midnight from a “save my pet” crowd funding group that somehow does not exist. No WePay, you will not pay whoever used you to try and steal money from us. Somehow you have become a third party channel for fraudulent activity.

matthew brown

The most unprofessional thing/place/site(whatever it is) to deal with. If you are lucky, you might get a standard response via e-mail 3-5 days later. They take your money, then sit on it for, well at least 2 months, and counting. I’m a small business and they took $3700 from my acct without even a phone call. They DO NOT use phones. Clearly because they don’t have any professionals there to handle any situations that they themselves created. They are a Chase company, and it makes me cringe that our government kept jokes like this heads above water, only for them to be crooks to the working man. Should have let them sink like the fat lazy garbage this outfit is.

Stay away – they are crooks. We process a high volume of orders, and we began noticing that our revenue records were not matching the deposits. Upon further inquiry, we found that they were in fact not depositing all of our completed transactions into our bank account. When we asked why, it took them 3 days to respond and then they said it was a glitch and that they would fix it. Well, that was the last I heard from them. They never fixed it and the issue kept happening. Repeated emails to them went unanswered so we immediately took our business to another payment provider and have had zero issues with our new payment provider since. In all total, it appears that WePay stole about $3,200 from us. We contemplated filing suit, but it would’ve been cost prohibitive to do so. WePay isn’t a Better Business Bureau member so even though we filed a grievance through that, they apparently ignored it. My advice, stay away from both WePay and UltraCart. UltraCart was the cart system we used which is owned by WePay, and so of course they were of no help whatsoever. They ignored us just like WePay did. WePay lost a lot of business with us.

WePay is a total scam. I use Freshbooks as my small business accounting platform. A client paid an invoice using a Visa credit card (not a debit card). I received an email that the payment was received from the client via Freshbooks. I then received an email from WePay stating that the “withdrawl” from my WePay account was denied. They couldn’t verify who I was, even though my business bank account is connected to Freshbooks AND WePay. They are now keeping my payment. They have NO customer support number, only email, which they do NOT respond to. Shame on you WePay.

Shame on WEPAY and shame on MEETUP for using this platform to collect contributions. I have contacted WEPAY through the Internet to get my contributions out. Mira from WEPAY requested screen shots after screenshots. She finally said go to a public computer and try since she couldn’t figure out why my verification was just clocking. Then today I reached out to Mira and it bounced back saying their procedure to replies changed and I have to start all over with my inquiry!!HORRIBLE – I will be reporting to BBB.

B.Lynne Hoff

About 4 months ago I started a GoFUndMe Campaign for a friend suffering from Leukemia and Bladder Cancer. His friends immediately donated over $2000.00 To date, we have been unable to recover these funds from WEPay via GoFUndMe. THe excuses range from unable to identify thru trouble with deposit to bank. In the meantime my friend has lost his car because of unable to pay AND I am helping with his medical bills while the money sits in his GoFUndMe account. I would NEVER use GioFUndMe/WEPay again!

Hugo Z

MightyCause (Razoo) uses WePay. MightyCause does not provide telephone support. Just online support. After taking & making so much money from charity fundraise, no support?!! So greedy and so lazy.

Tom Story Esq

Using a platform for estimates they added WePay Inc to add payment processing to the list of things they do provide me.

I never signed up for We Pay, I use another credit card transactions company. Well using a backdoor method with joist, We Pay is able to process your customers credit cards even if your not signed up with them.

I then get a Email, informing me they have over $10,000 worth of funds of mine and please verify my business and banking information. Well obviously $10k to some company in ca I’m going to want to retrieve my funds.

Follow all the steps to verify who I am and the credentials for my company to collect the funds they have collected through deception, making my customers think I process cards through them but I don’t.

To then have to email them 6 days later asking where my money is. Was I surprised when they finally got back to me with 4 emails in a row saying, first my company that’s been open for years, and my bank who I’ve had a company account for years and even have a loan from for my construction business could not be verify.

Since they could not “verify ” my bank or company information they have refunded all my customers and closed my account.

Funny, I wish that’s really what they did, they never returned my customers money, I’ve been receiving phone calls from 2 customers looking for in total about $10k processed through WePay Inc, now since we pay has not returned the money and I asked them to pay a diffeeent way, since the funds have not been returned it looks like I’m trying to scam them.

I am filling a Class Action lawsuit against

WePay Inc, for deceptive advertising amongst other things.

If you have been a victim of this WePay Inc scam please contact me, [email protected]

I would love to hear from you and my attorney can add you on the suite!!!

Lew Picardi

This is a SCAM entity. Stay away from using them in any way whatsoever. I have been getting charged monthly now for a year and cannot seem to stop their criminal activity. I changed credit card numbers but still get charges as they somehow obtain your new charge number. There is nothing but deceit, fraud and criminal activity coming from this company. I repeat this is a SCAMMING business and should be prosecuted as such!

Ann

I don’t think too highly of a company that charges fees for donations to an individual trying to raise money to pay medical bills after finding out they have cancer. This individual really needed the money, and wepay had to take a portion of it. What a terrible company to take much-needed funds from a poor woman. Not right at all. I hope people will realize what a ripoff company this is and stop dealing with them.

K

Do not use WePay. As a payment processor they allow software to utilize their platform that doesn’t work correctly, and their support defaults to lying about it. We use a donation platform that used WePay, and through that platform we needed to cancel all of our recurring donations. We cancelled them all in that system, and that system continued to submit charges to WePay. We contacted WePay who told us they couldn’t help with the cancellations, but then the vendor told us that the only way to solve their problem was for WePay to cancel the donations, even though WePay told us they could do nothing. As of this writing, they’re still stealing money from our donors regularly (which we then have to individually refund) but we can’t terminate our account because if we do that, we lose access to all reporting data which we may need for a future audit. This is incredibly anti-customer behavior not just to me as an organization, but to donors looking to support non-profits. They are literally engaging in theft and lying about methods to solve it. Stay far, far away from any platform that utilizes WePay!

Justin J Bartley

Worst decision I ever made was to use this company for my small business. They couldn’t care less about the customer or getting the funds to them. Biggest red flag should’ve been no phone number to speak to someone. Only an email. Wepay will never get another dime of my money

Brandon Willis

This company Customer Service is pathetic, they have had $13,000 of my money now for over two weeks and they won’t return my phone call and they don’t even have a Customer Service phone line. Never will I do business with them again or run any of my transactions through them them again. We are a multi million dollar company, they definitely won’t be getting anymore of our business, if I don’t get a contact by 2:00 Central time today, we will get a lawyers involved. Thanks, looking forward to hearing something back soon.

Charles Therriault